(1)")

")

Many entrepreneurs in Canada start out as sole proprietors. It’s simple, fast, and feels like the easiest way to begin. But as income grows and financial goals become more complex, that structure can start to hold you back.

This post explores the benefits of incorporating in Canada—from lower tax rates to better asset protection and long-term planning options.

⚠️ Think It’s Too Expensive or Complicated?

One common misconception is that incorporating takes thousands of dollars and requires a lawyer.

Not true.

You can register a federal corporation online for about $275 CAD, and it takes less than an hour if you have a name and structure in mind.

👉 Click here to access the federal incorporation portal

While legal or accounting help can be useful in complex situations, many business owners set up their corporation on their own.

🔄 Sole Proprietor vs Corporation

Here’s how they differ:

Sole proprietorship:

- You and your business are the same entity

- You’re personally liable for everything

- You pay full personal income tax on all profits

- You can’t easily transfer or sell the business

Corporation:

- It’s a separate legal entity

- You have limited liability

- You can access lower tax rates

- You can build, sell, or pass it on much more easily

One of the biggest benefits of incorporating in Canada is the ability to separate your business from your personal identity.

🧠 Key Benefits of Incorporating in Canada

Let’s break it down:

✅ Lower Tax Rates

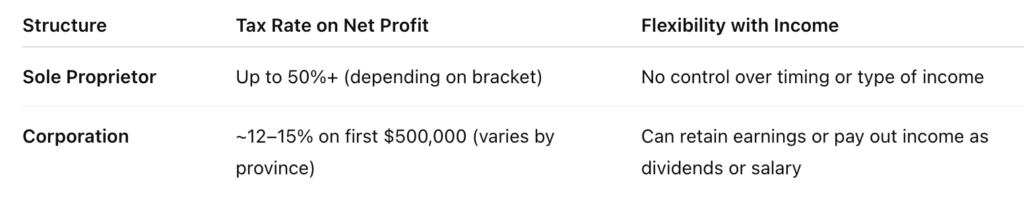

Small Canadian corporations usually pay around 12%–15% on their first $500,000 in income. Sole proprietors can pay up to 50%+, depending on the province and income bracket.

✅ Income Flexibility

You can leave money in the corporation, reinvest it, or choose how to pay yourself—through salary, dividends, or both. This flexibility lets you optimize taxes and cash flow.

✅ Professional Image

Incorporation can help your business look more credible to clients, partners, and lenders.

✅ Easier to Grow and Transition

Corporations can sell shares, raise capital, and continue beyond your lifetime. That makes succession and exit planning much smoother.

📊 Sole Proprietor vs Corporation Tax Summary

💼 Smarter Spending Through a Corporation

Corporations can deduct business expenses before calculating taxable income. That means they operate using pre-tax dollars, which goes further.

Common deductions:

- Home office (portion of rent, utilities, internet)

- Software and tools

- Travel and meals (business-related)

- Vehicle expenses

- Marketing and advertising

- Professional development

- Staff or family wages (if they work in the business)

These deductions reduce the corporation’s taxable income—something sole proprietors don’t always optimize.

🏠 Owning Assets Through a Corporation

One of the lesser-known benefits of incorporating in Canada is that corporations can own assets. That includes:

🏘 Real Estate

- Rental properties can be held in a corporation

- Expenses like repairs, taxes, mortgage interest, and upgrades are deductible

- Rental income is taxed at the lower corporate rate

- It separates liability from your personal finances

- You can use a holding company to build wealth more safely

🛡 Life Insurance

Corporations can also own participating whole life insurance policies. These policies can:

- Grow tax-sheltered cash value

- Act as a liquid asset for future opportunities

- Pass on a tax-free death benefit

- Reduce exposure in your personal estate

Owning assets like these in a corporation allows for cleaner accounting, legacy planning, and tax efficiency.

🧱 Building a Structure: OpCo + HoldCo

As your business evolves, you might consider creating two corporations:

- OpCo (Operating Company): where the day-to-day business happens

- HoldCo (Holding Company): owns shares in OpCo, holds profits, insurance, or real estate

Why do this?

- You separate risk from wealth

- You can move profits up into HoldCo for investing

- It supports succession planning and intergenerational wealth transfer

This isn’t just for big corporations—it’s a common strategy for family-run businesses and small business owners planning for the future.

🧬 Adding Trusts for Long-Term Planning

Incorporated businesses can also work with trusts to add another layer of protection and control.

Trusts can:

- Own shares in your corporation

- Split income to multiple beneficiaries

- Avoid probate

- Preserve wealth within your family

Again, these tools only become available when the business is separated from your personal finances through incorporation.

📝 Final Thought

This article is for informational purposes only and doesn’t constitute legal, tax, or financial advice.

That said, the benefits of incorporating in Canada are hard to ignore. It’s a powerful step toward building financial freedom, tax efficiency, and long-term flexibility.

💬 Want to Explore Your Options?

If you’re wondering whether it’s time to incorporate—or how to use a corporation to build wealth—we’re here to help.

Book a no-pressure clarity call to explore your structure, goals, and opportunities.

👉 Click here to book your Freedom Family Financial call.

Let’s build something that supports your family, your future, and your freedom.